Navigation » List of Schools, Subjects, and Courses » Accounting 3200A – Intermediate Financial Accounting & Reporting I » Homeworks » Chapter 4 Homework

With Answers Good news! We are showing you only an excerpt of our suggested answer to this question. Should you need our help in customizing an answer to this question, feel free to send us an email at  or chat with our customer service representative.

or chat with our customer service representative.

Chapter 4 Homework

Chapter 4 Homework

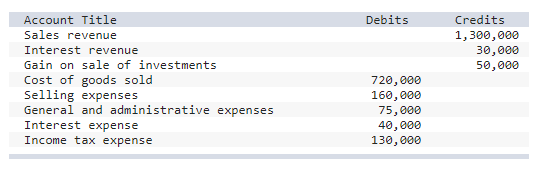

1. The following is a partial trial balance for the Green Star Corporation as of December 31, 2021:

There were 100,000 shares of common stock outstanding throughout 2021.

Required:

Prepare a single-step income statement for 2021, including EPS disclosures.

Prepare a multiple-step income statement for 2021, including EPS disclosures.

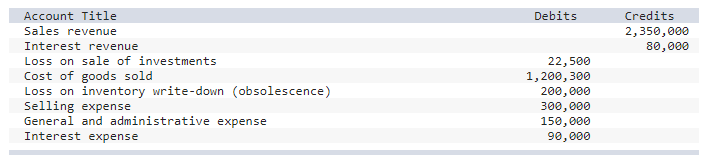

2. The following is a partial trial balance for General Lighting Corporation as of December 31, 2021:

There were 160,000 shares of common stock outstanding throughout 2021. Income tax expense has not yet been recorded. The income tax rate is 25%.

Required:

Prepare a single-step income statement for 2021, including EPS disclosures.

Prepare a multiple-step income statement for 2021, including EPS disclosures.

3. The trial balance for Lindor Corporation, a manufacturing company, for the year ended December 31, 2021, included the following accounts:

The gain on debt securities is unrealized and classified as other comprehensive income. The trial balance does not include the accrual for income taxes. Lindor’s income tax rate is 25%. There were 1,500,000 shares of common stock outstanding throughout 2021.

Required:

Prepare a single, continuous multiple-step statement of comprehensive income for 2021, including appropriate EPS disclosures. (Round EPS answer to 2 decimal places.)

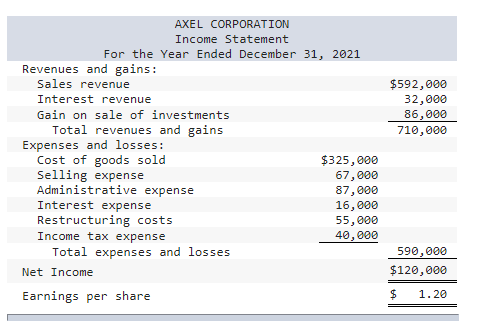

4. The following incorrect income statement was prepared by the accountant of the Axel Corporation:

Required:

Prepare a multiple-step income statement for 2021 applying generally accepted accounting principles. The income tax rate is 25%. (Amounts to be deducted should be indicated with a minus sign. Round EPS answer to 2 decimal places.)

5. Chance Company had two operating divisions, one manufacturing farm equipment and the other office supplies. Both divisions are considered separate components as defined by generally accepted accounting principles. The farm equipment component had been unprofitable, and on September 1, 2021, the company adopted a plan to sell the assets of the division. The actual sale was completed on December 15, 2021, at a price of $600,000. The book value of the division’s assets was $1,000,000, resulting in a before-tax loss of $400,000 on the sale.

The division incurred a before-tax operating loss from operations of $120,000 from the beginning of the year through December 15. The income tax rate is 25%. Chance’s after-tax income from its continuing operations is $550,000.

Required:

Prepare an income statement for 2021 beginning with income from continuing operations. Include appropriate EPS disclosures assuming that 100,000 shares of common stock were outstanding throughout the year. (Amounts to be deducted should be indicated with a minus sign. Round EPS answers to 2 decimal places.)

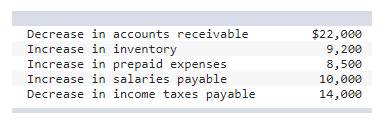

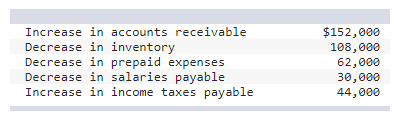

6. Cemptex Corporation prepares its statement of cash flows using the indirect method to report operating activities. Net income for the 2021 fiscal year was $624,000. Depreciation and amortization expense of $87,000 was included with operating expenses in the income statement. The following information describes the changes in current assets and liabilities other than cash:

Required:

Prepare the operating activities section of the 2021 statement of cash flows. (Amounts to be deducted should be indicated with a minus sign.)

7. Chew Corporation prepares its statement of cash flows using the indirect method of reporting operating activities. Net income for the 2021 fiscal year was $1,250,000. Depreciation expense of $140,000 was included with operating expenses in the income statement. The following information describes the changes in current assets and liabilities other than cash:

Required:

Prepare the cash flows from operating activities for 2021. (Amounts to be deducted should be indicated with a minus sign.)